These are rough times. We will bring you regular updates on Covid-19 and how it may impact your finances through this Coronavirus Dashboard.

Tax Compliance Updates

Income Tax

- Ministry of Finance to release pending Income Tax refunds up to INR 5 Lakh & all pending GST and Customs refunds. A highly appreciated move during crucial times. Are you expecting a long due refund? Check your Income Tax Refund status here.

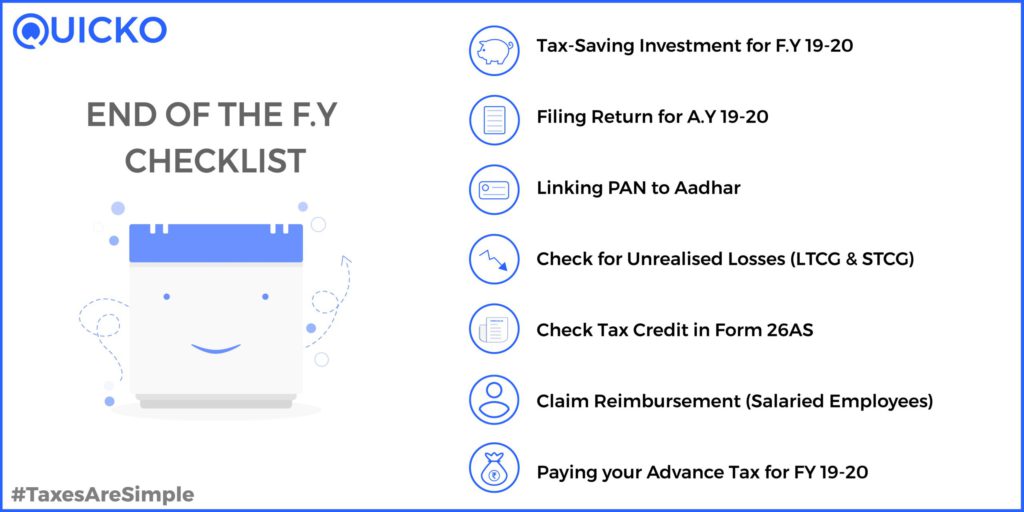

- The last date for filing Income Tax Returns for FY 18-19 extended to June 30 from March 31 due to the Covid outbreak.

- Subsequently, all compliances under the Income Tax Act, Wealth Tax Act, Benami Transaction Act, Vivaad se Vishwaas, have been extended to June 30, 2020.

- May 15, 2020, Last date for Employers to issue Form-16.

- June 15, 2020, Quarterly Form 16A.

- June 30, 2020, Last date for investing under chapter VIA.

- June 30, 2020, Last date for filing Belated Tax Return for FY 2018-19.

GST

- The last date for filing March-April-May GST returns extended to June 30, 2020.

- No interests, penalty or late fees to be charged for late filing of GST Returns for companies with Turnover of INR 5 Crore of less.

TDS

- Interests charged on delayed deposits of TDS reduced to 9% from 18%.

- April, 30, 2020, Last date for TDS Deposits.

- May 15, 2020, Due date Q4 TCS Deposit.

- May 31, 2020, Due date for Q4 TDS Return

- June 7, 2020, Due date for TDS Deposit.

- June 15, 2020, Quarterly TDS Certificate

ROC Compliance

- June 30, 2020, Last date for linking PAN with Aadhar.

- Mandatory requirement of holding board meetings relaxed by 60 days, this relaxation is for the next two quarters.

- Newly incorporated companies get an additional 6 more months to file the declaration.

- (MSMEs) The threshold for default under IBC raised to INR 1 Crore from INR 1 Lakh.

Economic Package Updates and other Financial Updates

Economic Package

March 26, 2020, For the next three months, the Government to pay the full contribution to EPF for companies with 100+ employees and 90% earning below INR 15,000 per month.

- FM announced Economic Package of INR 1.7 Crore.

- Insurance cover of INR 50 Lakh per person announced for Doctors, Paramedic and Healthcare Workers.

- 20 Crore women Jan Dhan Yojna account holders to get INR 500 every month for the next 3 months.

- 8.69 Crore farmers to get INR 2000 under PM-Kisan Yojna

- FM announces an ex-gratia of INR 1,000 for 3 Crore poor senior citizens.

- Under PM Garib Anna Yojna, 80 Crore poor people to get 5 Kg grains per month for 3 months.

Other Financial Updates

April 3, 2020, World Bank approves and emergency fund of $ 1 Billion to India.

April 1, 2020, Financial year 2020-21 starts in India.

March 27, 2020, In a Press Conference, RBI Governor announced the reduction in Repo rates by 75 bps to 4.4%. Earlier the Repo Rate was 5.15%.

- The Reverse Repo rates have been cut by 90 bps to 4%.

- A liquidity boost of INR 3.7 Crore announced by the RBI.

March 20, 2020, The IRS declared that US taxpayers can file their taxes until July 15. The previous deadline was April 15.

March 19, 2020, Prime Minister Narendra Modi announces an ‘Economic Task Force’ for providing Economic packages to MSMEs and other worst-hit sectors. Read More.

March 18, 2020, Several companies, banks, NBFCs have refused to comply with the summons of the Income Tax Department, stating COVID-19 as a reason.

March 14, 2020, GST on Repair and Overhaul on aircraft reduced to 5% to boost the badly affected Aviation Industry.

COVID-19 Latest Updates

April 14, 2020, Narendra Modi has announced extension of the complete lockdown of the country till May 3.

April 14, 2020, Total cases in India rise to 10,363. As per Ministry of Health and Family Welfare:-

- Active cases : 8,987

- Cured/Discharged : 1036

- Deaths : 339

- Migrated : 1

April 12, 2020, India is planning to restart some manufacturing after April 15 to help offset the economic damage of a nationwide coronavirus lockdown, two government sources said, even as it weighs extending the lockdown.

April 12, 2020, China’s reports 108 new COVID-19 cases. Fears for a second wave arise.

April 9, 2020, India crosses the 5,700 mark of total positive cases. Odisha- first state to extend lockdown till 30th April.

April 6, 2020, Doubling rate of COVID-19 at 4 days as India registered 4367 infected cases. 330 Individuals have recovered.

April 3, 2020, Asia’s biggest slum, Dharavi registers 3 new cases.

April 1, 2020, White House projected 1,00,000- 2,40,000 deaths due to COVID-19. New York became the newest epicenter of the Virus registering over 1,500 deaths alone.

March 31, 2020, As many as 2000 Individuals found at the Nizamuddin area. Individuals were a part of Tablighi-Jamat.

March 30, 2020, Total number of infected Individuals in India reaches 1200 and recovered Individuals reach 102. Sadly, 29 Individuals have deceased.

- Train Coaches being prepared as Isolation Wards for COVID-19 patients as cases continue to surge.

March 28, 2020, Thousands of Migrant laborers accumulated at Delhi’s Vasant Vihaar Bus Terminal wanting to go back to their native land.

March 25, 2020, Prince Charles of the British Royal Family tested positive for Covid-19.

March 24, 2020, PM announces complete lock-down for 21 days i.e until April 14, 2020. INR 15,000 Crore allocated for Healthcare systems.

- Tokyo Olympics to be held in the Summer of 2021

March 23, 2020, India has suspended operations of domestic schedule commercial airlines effective from the midnight that is 23.59 hours IST on 24/3/2020

- COVID-19 causing mass hysteria among investors. BSE hit its 10% lower circuit level after reopening to a 45-minute halt. S&P BSE lost 3,600 points.

March 22, 2020, The Government in India halts passenger trains till 31st March 2020.

Match 19, 2020, PM Narendra Modi addressed the nation and announced a Janta Curfew on Sunday. An ‘Economic Package’ was also announced by PM Modi.

March 18, 2020, Indian Army reports its first case of Covid-19.

March 12, 2020, India registers it’s first confirmed death from Covid-19. The 76-year-old man from Karnataka had traveled from Saudi Arabia.

March 11, 2020, WHO declares Covid-19 as a ‘Pandemic’, urges countries to take proactive measures.

January 30, 2020, India registers its first Covid-19 case. Quarantined Individual from Kerala. The patient is a student at Wuhan University, China.

Quicko Updates

March 21, 2020, Being a responsible team of developers, chartered accountants and content creators, we have decided to Work From Home. It does not dilute our commitment to make Taxes Simple For All.

March 20, 2020, Quicko’s celebrates partnering with HDFC Securities, with https://hdfcsecurities.quicko.com/. The official tax compliance partner for HDFC Traders.

March 20, 2020, Taxes for Traders are now simpler. Quicko announced https://trader.quicko.com/.