The Budget 2020 was announced on 1st February 2020 with the aim to revive our slowing Economy. Introducing an optional Tax Regime was the biggest highlight. However, other notable announcements having an effect on Businesses were also made. Let’s take a look!

From the Business point of view, these announcements stole the show!

- Option to choose between Current Tax Regime and New Tax Regime

- TDS For Professional and Technical Services u/s 194J

- Taxability of Dividend Income

- Taxability of sales through E-commerce platforms

- Applicability of Tax Audit

- Extension in the due date to file Income Tax Return in case of Tax Audit

Let us look at them one by one.

Option to choose between Current and New Tax Regime

Finance Minister Nirmala Sitharaman announced an ‘Optional’ Tax Regime for Taxpayers. This Tax Regime allows Taxpayers and Businesses to have more take-home income.

Several Deductions like Leave Travel Allowance and Standard Deduction on Salary were canceled out in the New Tax Regime. But deductions like Voluntary Retirement Schemes and rebate u/s 87A were still covered.

The New Tax Regime aims to give more financial freedom to Individuals and Businesses without a compulsion to invest in sections like 80C to avail Tax benefit.

TDS For Professional and Technical Services u/s 194J

Section 194J of the I-T Act deals with TDS on payments for services such as — fees for professional services, fees for technical services, royalty, and non-compete fees. The TDS applicable for both was at 10%. However, Finance Minister Nirmala Sitharaman announced changes of TDS on the fee for technical services.

The TDS for Technical services was slashed from 10% to 2%. However, for all other services such as professional services, royalty, non-compete fees etc, TDS Rate is still 10%. Thus, it is important to understand the difference between technical services and professional services.

It is hoped that this change will reduce litigations arising due to the difference in opinion between assessee and tax officers to deduct TDS on certain services under 194C at 2% or 194J at 10%.

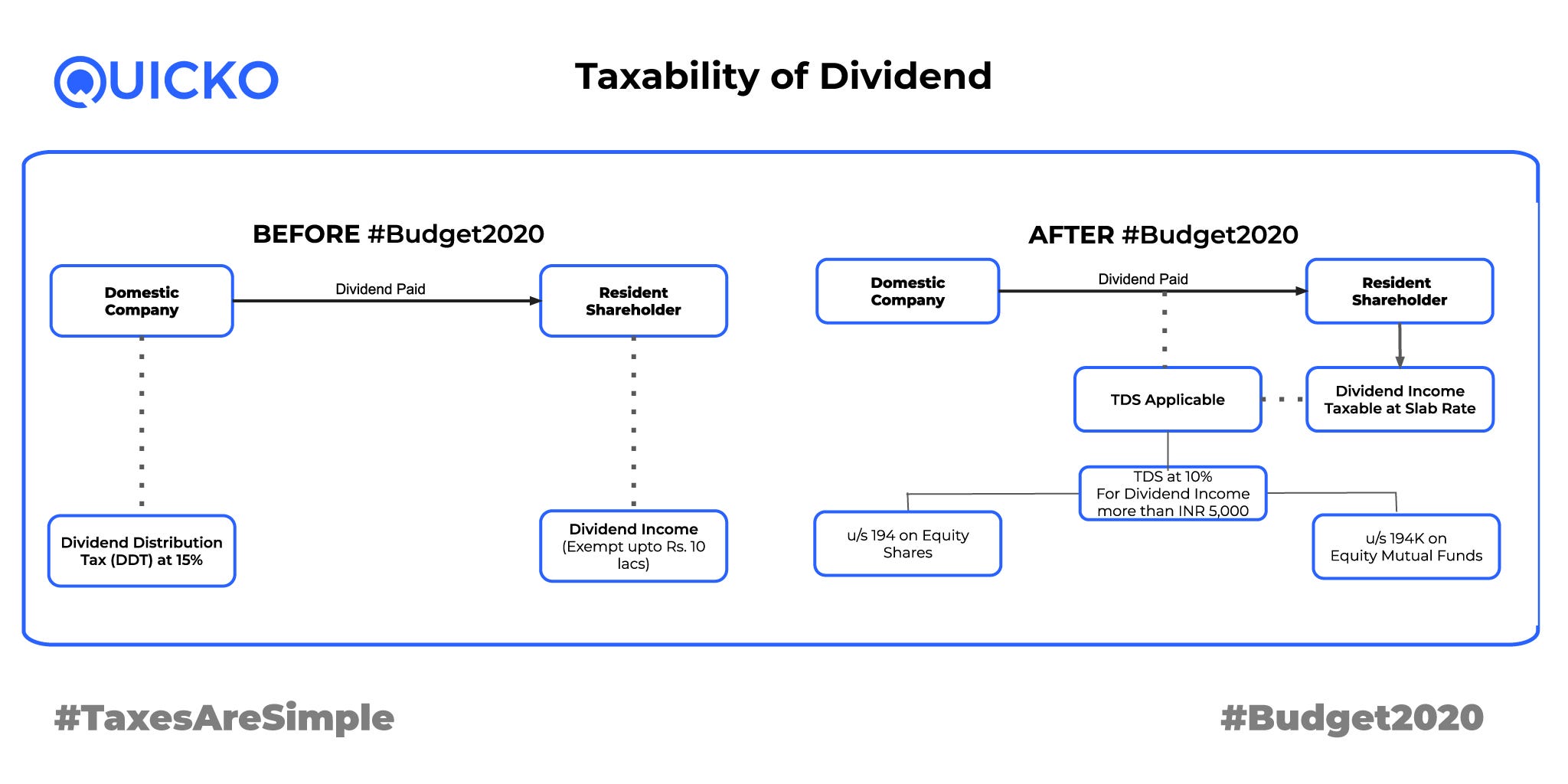

Taxability For Dividend

To understand the change made, we need to have a History Lesson!

Up to F.Y. 2019–20

Domestic Companies were liable to pay DDT (Dividend Distribution Tax) at 15% on the amount of Dividend distributed to a shareholder. This dividend included

- Dividend on equity shares

- Dividend on equity mutual funds.

The dividend income up to INR 10 Lakh u/s 10(34) was exempt in the hands of the shareholder. Since that income was not taxable, there was no applicability of TDS.

F.Y 2020–21 Onwards

Section 115-O has been abolished in the Budget. Thus, Domestic Companies are not liable to pay DDT (Dividend Distribution Tax) on the Dividend distributed on Equity Shares/Mutual Funds to the shareholder.

Now that the Dividend isn’t paid by the company, it becomes natural that it becomes taxable in the hands of the shareholder as per the applicable slab rate…What a Bummer! Ergo, TDS on dividend income was introduced.

In Budget 2020, these changes were announced to introduce TDS on Dividend Income:-

- Amendment of Section 194

Domestic Company should deduct TDS @ 10% on dividend on equity shares in excess of INR 5,000.

- Introduction of Section 194K

Asset Management Company (AMC) will deduct TDS @10% on dividend on equity mutual funds in excess of INR 5,000.

Taxability For E-commerce platforms

Since the last few years, we have witnessed the emergence in popularity of E-Commerce Platforms. Websites like Amazon, Myntra are slowly but surely reforming how we shop! Prior to the Budget, TDS wasn’t anywhere in the picture. Income earned by E-Commerce Sellers was just liable to be taxed as per income tax slab rates. But on 1st February, FinMin announced that TDS shall be deducted on Income from E-Com platforms.

Individuals and HUFs will enjoy exemption from TDS until Sales of INR 5 Lakh in a year. However, if the gross sales exceed INR 5 Lakh, TDS is required to be deducted at 1% if PAN or Aadhar is provided by the e-commerce seller. Subsequently, if an E-Com seller does not provide PAN or Aadhar, the e-commerce operator needs to deduct TDS @ 5% on the gross sales.

For any business other than Individual or HUF, TDS is required to be deducted @ 1% irrespective of the sales amount. TDS is required to be deducted at 5% in the absence of PAN.

Applicability of Tax Audit

Prior to the Budget 2020, Tax Audit was applicable to an assessee whose turnover was more than 2 Crore or if turnover was less than 2 Crore, the profits were less than 6% of turnover.

Under Budget 2020, the limit of 2 Crore was increased to 5 Crore for assessee who fulfills the below condition:

- Cash Sales does not exceed 5% of Total Sales

- Cash Expenses does not exceed 5% of Total Expenses

Refer to the image below for further clarity

Extension in the due date to file Income Tax Return in case of Tax Audit

Before Budget 2020, the date of submitting the Tax Audit Report and Income Tax Return was the same i.e on 31st July. However, in order to reduce chaos and to give valuable breathing time to the Businesses and Finance Department, the Due date for submitting Tax Audit Report was extended.

The date to submit the Tax Audit was extended to 31st September 2020. Likewise, the date for filing Income Tax Returns was also updated to 31st October 2020.

It is hoped that this extension will help avoid the usual delays in the Tax Auditing and Return filing process.

Hey @TeamQuicko

Can I opt out of New Scheme once opted in???

If I want to opt for the New regime but had told my employer that I am choosing the existing one, can I select new tax regime while filing ITR??

Hey @riya_gupta

An individual having salaried income and no business income has the option to choose between the old and new tax regimes every year i.e. he/she can switch regimes from year to year.

However, individuals having business income are not eligible to choose between the new and old tax regime every year. Once they have opted for the new tax regime, they only have a one-time option of switching back to the old tax regime in their lifetime.

Once they switch back, they will not be allowed to opt for new tax regime again.

Hey @TanyaChopra

If you have opted for old tax regime with your employer for TDS on salary, and plan to opt the new tax regime at the time of filing ITR, then you can do that by filling the new form i.e. 10-IE.

Can full-time traders claim expenses like Broker charges STT, GST + other expenses like computer buy for trading, internet connection bill etc under new tax slabs?