What Stays & What Goes

A major chunk of deductions and exemptions are removed under the New Tax Regime. The important tax breaks that will no longer be available under the New Tax Regime include Chapter VI-A deductions like 80C, 80D, 80DD, 80U, 80TTA/TTB, 80E, HRA, LTA and interest on Housing Loan. There are a few deductions that can still be claimed!

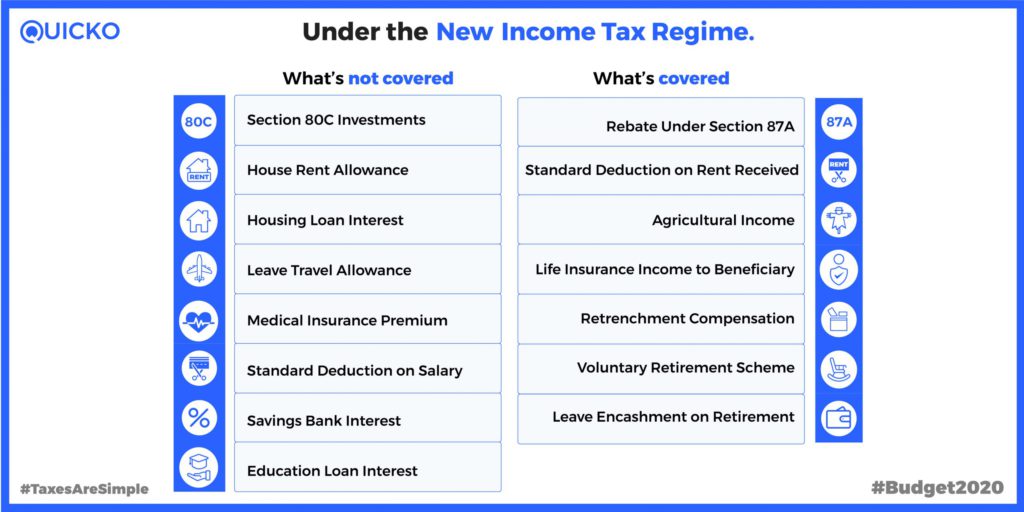

Look at a list of all the deductions under the New Tax Regime which the Budget 2020 covers and does not cover!

Deductions we have to part ways with:

The most popular deductions of Chapter VIA have been abolished-

All deductions except 80CCD(2) and 80JJAA have been removed. The sections removed are:

- Investments – 80C, 80CCC, 80CCD(1), 80CCD(1B), 80CCG

- Medical Insurance – 80D, 80DD, 80DDB, 80U

- House Property – 80U, 80E, 80TTA/TTB, 80EE, 80EEA

- Donations – 80G, 80GG, 80GGA, 80GGC- Donations

- 80IA, 80IAB, 80IB, 80IBA, 80IC, 80JJA, 80QQB, 80RRB.

These include deductions on Life Insurance Premium, School Tuition Fees, Housing Loan Principal, Medical Insurance Premium & other investments like ELSS, NPS, and finally the majorly claimed Provident Fund.

PPF might still continue to be the most popular fixed-income product, irrespective of these changes.

Investment in PPF can no longer be claimed. The exemption on the interest earned through PPF as well as the total sum received at maturity is exempt from tax. This will give a boost to long-term investment planning.

The huge deduction of medical insurance premium has been removed, too:

A deduction of INR 25,000 can be claimed under section 80D on insurance for self, spouse and children. An additional deduction for insurance of parents is also available. This depends on the age of the parents. The maximum deduction available u/s 80D is Rs. 1,00,000. This can only be claimed in the Old tax Regime.

Interest from savings bank account abolished:

This exemption is claimed under Section 80TTA and 80TTB. No more deductions in respect to interests from savings accounts is allowed. This applies to both senior and non-senior citizens.

No deduction for interest paid on education loan:

Under Section 80E, you can claim deduction on interest paid on education loan. It does not have any maximum limit. However, it can be claimed for a maximum period of 8 years under the Old Tax Regime. But this is also being excluded from the list of tax-deductions under the New Tax Regime.

Salaried individuals can no longer claim a large number of exemptions:

- House Rent Allowance (HRA) is normally paid to salaried individuals as part of their salary. This could be claimed up to a certain limit if the individual is staying in rented accommodation.

- Leave Travel Allowance (LTA) is the amount paid by the employer to an employee for travel expenditure with or without family within the country exemption. This is currently available to salaried employees twice in a block of four years.

- The Standard Deduction of INR 50,000 is currently available to salaried individuals. It can no longer be claimed under the New Tax Regime.

- Transport Allowance and Entertainment Allowance are exempt from taxes too.

- Professional Tax is usually around INR 200 a month, with the maximum payable in a year being INR 2,500. The exemption on the same is also not available under the New Tax Regime.

- Housing Loan Interest paid for self-occupied properties can be claimed as a deduction under income from house property. This results in a loss from house property. This loss can be set off against salary income thereby reducing the taxable income and in turn the net tax liability.

A few other exemptions which were removed:

- Exemption available on Clubbing Income of Minor Child up to INR 1,500.

- Deduction available on Family Pension u/s 57(iia). The exemption of INR 15,000 or 1/3rd of the amount received, whichever is less, is available.

- Exemption in respect of Units establishment in SEZ u/s 10AA

Deductions that stay:

A little something under Chapter VIA can still be claimed:

These include Employer’s Contribution to Provident Fund (EPF) and deduction under section 80JJAA i.e. deduction for employment of new employees.

Rebate Under Section 87A:

This rebate is limited to INR 12,500. This means that if your total income is lower than INR 5,00,000 then the tax payable will be your rebate under section 87A.

Standard Deduction on Rent Received still remains:

Standard Deduction on Rent Received is 30% of the Net Annual Value of Income from House Property. This 30% deduction is allowed even when your actual expenditure on the property is higher or lower.

Interest on Housing Loan for Let Out Property:

This deduction can still be claimed under the New Tax Regime unlike the Interest on housing loan for self-occupied property. However, you can only claim Interest upto the amount of Rental Income received. You can not set off or carry forward the loss of Interest paid on Housing Loan.

Agricultural Income is not taxable. It is not counted as a part of an individual’s total income. However, the ‘state’ government can levy tax on agricultural income if the amount exceeds INR 5,000 per year.

No compromise on retirement allowances to salaried individuals:

The following exemption are still allowed under the New Tax Regime:

- Amount received/receivable on voluntary retirement or termination of service or Voluntary Retirement Scheme (VRS) is a method used by companies to reduce surplus staff. It is subject to exemption up to INR 5,00,000. The amount received up to INR 5,00,000 will be exempted and the balance amount will be taxable in the hands of employees under the head salary.

- Retrenchment Compensation is the financial compensation by the employer to an employee on terminating the employee’s job. This compensation which is received by a workman is exempt. It should not exceed the sum calculated on the basis provided in Section 25F(b) of Industrial Disputes Act, 1947 or any such amount as is specified by the Central Govt.

- Leave Encashment on Retirement is the amount of money received by an employee in exchange for a period of leave not availed. This amount is exempt from tax, subject to certain conditions and up to a maximum amount of INR 3 lakh.

- Commuted Value of Pension & Death-cum-retirement gratuity are other deductions which haven’t been abolished.

Few of the the exemptions which can still be claimed by the salaried individuals are Food Coupons and Gifts from Employer. Also Tax paid by employer on non-monetary perquisite can be claimed.

A few other exemptions which haven’t been removed:

- Life Insurance Premium received by the beneficiary is fully exempted from taxes

- Interest Received on Post Office Savings Account u/s 10(15) is exempt from taxes up to Rs.3,500 for single accounts and up to Rs.7,000 for joint accounts

- Money received as scholarship for education

- Cash received as awards constituted in public interest

- Short-term withdrawals and maturity amount from the National Pension Scheme (NPS)

- Interest and maturity amount received from PPF

- Interest and payment received from Sukanya Samriddhi Yojana

Budget 2020 made some really important changes to the Tax Regime. Taxpayers have two options. They can go with the New Tax Regime or the Old Tax Regime. There is nothing to worry about. Keep in mind the above. Select the suitable regime for FY 2020-21 so that maximum benefits can be derived. As a result your employer can deduct correct TDS once you have decided between the two.