Indians have always been considered as business-minded people. In India’s recent history, we have moved from an agriculture-based economy to a service-based economy. Startups have really been major contributors in doing so. However, making India a ‘startup-friendly‘ country will be our biggest challenge and biggest blessing altogether to achieve the $5 Trillion Economy landmark.

India has always encouraged startups. We have always tried to create a fertile environment for startups and businesses. Every year the Budget has ample announcements that enable startups to flourish.

Let us look at how the Budgets have treated their favorite prodigy- ‘Startups’ so far…

Budget 2018

Budget 2018 felt well-intentioned but partly fulfilled expectations. The Government made several announcements that made startups happy.

Prior to the Budget, Startups with a valuation of INR 50 Crore or more were required to pay corporate tax of 25%. The Government realized that this tax wasn’t allowing startups to grow at full potential and so they decided to increase the minimum valuation requirement to INR 250 Crore. However, we still lack behind in terms of the corporate tax. For Instance, the corporate tax in the USA and China is 21% and 20% respectively.

In conjunction with the previous announcement, Late Finance Minister Arun Jaitley gave startups another reason to be happy by announcing INR 1300 Crore for the telecom sector and digitizing India. It was a major problem for startups when they couldn’t grow due to a lack of proper Infrastructure. Surely, they would have sighed relief.

Have you heard the Quote, “Universe always balances itself out”? This quote was felt hard by the startups as they kept waiting for relaxation on Angel Tax but it never happened. One of the major reasons why Budget 2018 was criticized was because of the Angel Tax. Even in the pre-Budget predictions, think tanks had predicted relaxation on the issue. The Angel Tax issue was like the ‘Long Night‘. Surely this was a major Pain Nerve for startups.

Budget 2019

Just like in Game of Thrones, Jhon Snow did eventually defeated the ‘Night King‘. The feeling that he would have felt couldn’t be compared to the euphoria that Startups felt when Angel Tax was rationalized. CBDT came out with a notification in which startups would be allowed a retrospective effect on an exemption.

AOs will be required to get permission from its reporting officer and senior before scrutinizing any unregistered startup. Also on the Angel Tax front, an exemption was given u/s 52(2)(viib) to startups funded by Category-II AIF.

Budget 2019 announced an extension of 2 more years u/s 54GB. It allows exemption on Land Gains to Individuals and companies who used that amount to invest in a Startup. This announcement incentivized founders for funding in startups. Apart from that, the Government announced the extension of the Startup India Scheme up to 2025…two home-runs for startups!!

To boost the market for Electric Vehicles, reduced GST and IT rates were announced for Individual buyers and business owners. Also, the Government proposed 100 incubation centers which aimed at helping over 75,000 agriculture-based entrepreneurs. And 100% FDI was announced in the Insurance and Single Brand Retail sector.

It is safe to say that Budget 2019 was able to release the entrepreneurial spirit for startups…

Budget 2020

This year’s Budget was a special one! Often termed as a ‘Do-or-Die’ Budget, Nirmala Sitharaman’s take on the Economy was worrying to some folks.

But it still had a lot going for the startups. To address the concerns on tax holiday for startups, Section 80IAC was amended. The maximum turnover limit for startups to claim these deductions was increased to 100 CRore from 25 Crore. Along with that, the time limit to claim this deduction is also extended to 3 out of 10 previous years from 7 previous years.

One of the biggest announcements was the change in Tax Audit Applicability u/s 44AB. In FInMin’s bet to digitalize India, she announced an increased turnover limit from 1 Crore to 5 Crore, provided your cash sales and expenditures are less than 5% of total sales and total expenditure. Keep in mind, the due date for ITR filing of taxpayers to whom tax audit is extended from September 30 to October 31.

Hey, Tax Audit Applicability is usually a mind-bender for most people. This is why we have a Blog that will simplify Tax Audit for you. No more Tax Audit for Business/Trading Income having Turnover up to INR 5 Cr… Is it true?

Changes were announced for ESOPs as well. Earlier ESOPs were taxed twice-at the time of exercising ESOPs and at the time of selling shares. But now employees have been given relief by way of deferment of tax at the time of exercising options. This means an employee of startups who are exercising their ESOPs may have to pay tax at a later date i.e at the time of exit from the company or when they sell their shares or after 5 years of ESOPs being allocated. This announcement is especially important for startups as they can attract skilled talent with ease.

P.S If you wish to learn more about ESOPs and it’s taxability, we have a detailed article on How ESOPs are taxed in the hands of an Employee?

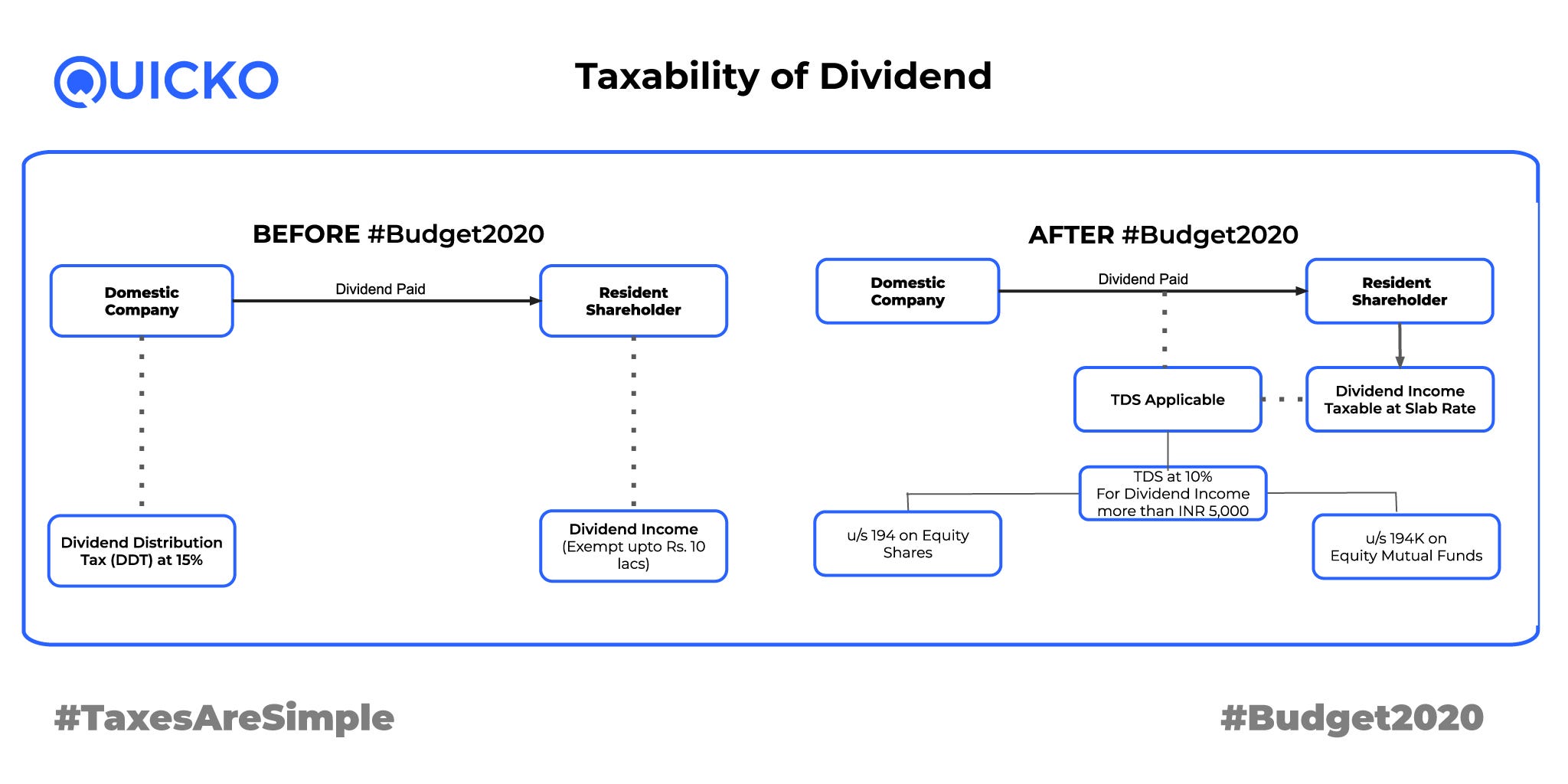

Since it was announced that DDT for companies will be abolished, startups will now have less tax compliance. But as DDT isn’t taxable in hands of companies/startups it naturally becomes taxable in the hands of shareholders. So, the impact of DDT being abolished can be left for speculation.

On the Corporate Tax front, great relaxation was given to startups and companies. The Corporate Tax rate for existing companies is reduced to 22% from 25% and the tax rate for Startups in the manufacturing sector was announced at 15%…..Rejoice Startups!!

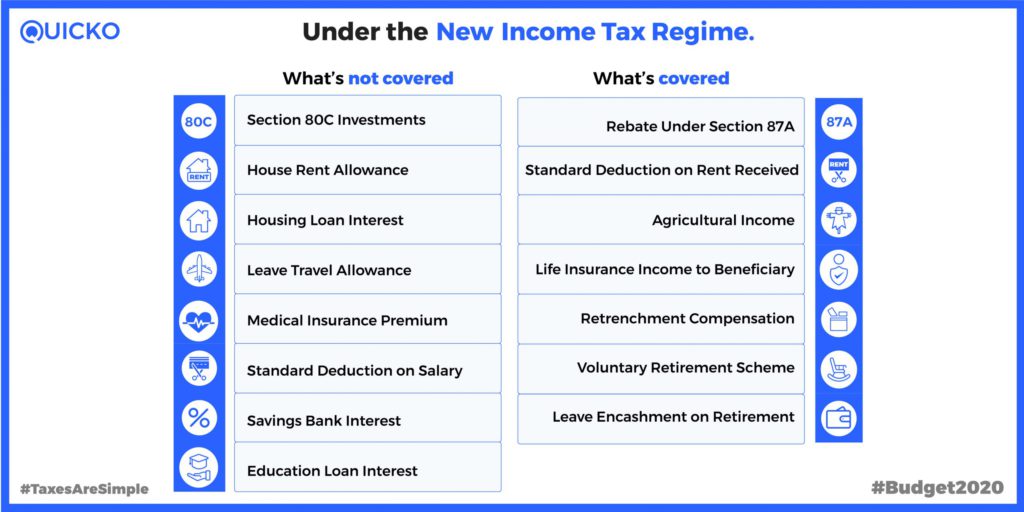

However, the introduction of the ‘Optional New Tax Regime’ has created confusion not only in the minds of salaried individuals but also aspiring Startups.

So far we’ve talked in the context of startups, but their employees are scratching their heads over the ‘Old Regime vs New Regime confusion’. To ease out the confusion we took the liberty of doing some research for your better understanding….take a look- Budget 2020: Current Tax Regime vs New Tax Regime causing a stir for salaried Individuals!

Our take…

We feel that with every Budget, the ease of doing business in India is getting better. Well, the Government reduced the Corporate Tax rate for startups. But if we really want to compete on all fronts at the global level, and need to focus more on providing a fertile ground for our startups to grow.

We still lack in terms of proper infrastructure which could facilitate a steady growth of startups. However, as the famous saying goes, “Rome wasn’t built in a day“.

It is safe to say that we have a mountain to climb, and judging by the trend, the Government will continue to give paramount importance to startups.

All looks good from here…