FM Nirmala Sitharaman announced the Budget 2020 on 1st February and made groundbreaking changes. Trying to target tax evasions by changing Residential Status conditions.

Four major changes were proposed in regard to the Residential Status.

- Criteria for determining residential Status Changed

- Change in RNOR

- New Clause added to Section 6 IA

- Change in the Dividend Distribution Tax (DDT)

Criteria for determining Residential Status changed

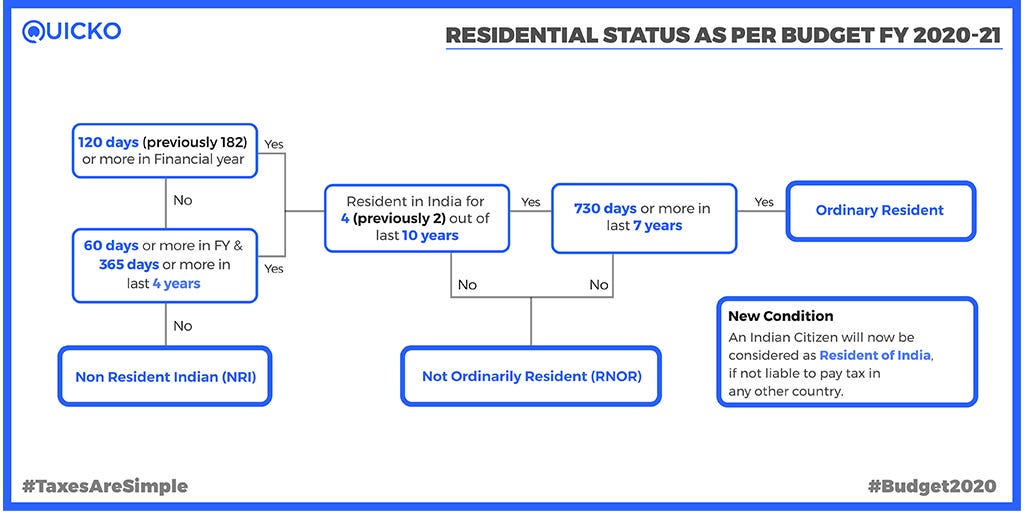

Prior to the Finance bill 2020, Individuals staying in India up to 181 days were not classified as Resident. Ergo avoid paying Taxes.

High Networth Individuals leveraged this to avoid paying tax on income earned in a foreign country. This was because they were never deemed a Resident.

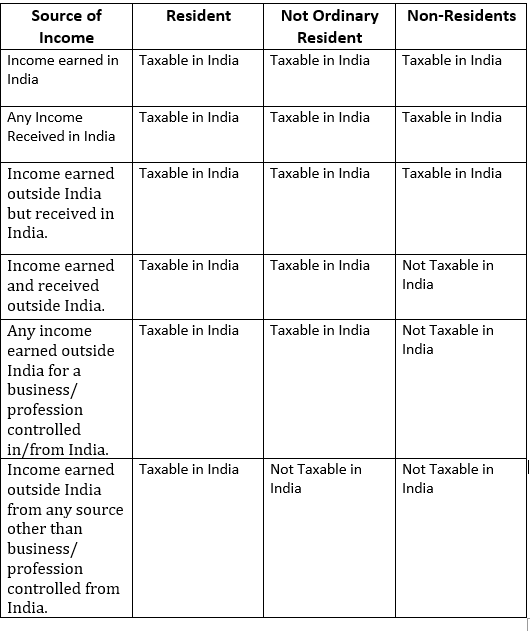

Once an individual is deemed a Resident, the income that accrues or arises outside India is also Taxable In India. This loophole was amended in the Budget 2020.

The Primary condition of 182 days for determining Residential Status has been changed to 120 days in the Union Budget 2020. This change would mean that Indian nationals Residing outside India will be deemed a Resident of India — if they stayed 120 days in a financial year.

Following this revision, the number of people who qualify for being a Resident of India will increase. Subsequently, Tax Revenue will increase.

Change for RNOR

Along with Government tightening the grip on Residential Status Criteria, it also gave a breather to some ‘genuine cases’.

Earlier to be an RNOR (Resident but Not Ordinary Resident) of India, one had to be a Resident for 2 out of 10 Previous Years and had to be in India not more than 729 days in all these years.

In Finance Bil 2020, the requirement of being a Resident was increased to 4 out of 10 Previous Year. So people who genuinely visit the country on personal visits like meeting family, or vacations — should not worry.

New Clause added to Section 6 IA

Any Indian Citizen will be deemed as a Resident of India if he/she isn’t a Resident in any other country.

Now, Indian Citizens that managed to evade taxes on Foreign Income — since they were not a Resident of any country — will be deemed as a Resident of India. They will now be liable to pay tax in India.

Another key change announced that if an Individual is a Deemed Resident of India, he/she will be required to disclose information of all the Assets and Finances in a foreign land. Individuals failing to do so will be listed under the Black Money Act. This change is expected to help curb the outflow of unregistered Income outside India.

Changes on similar lines have been made in the US. For instance: Tech Giant Apple Inc avoided paying taxes in the US, as their establishments were in countries with zero tax or very less tax. The US Finance Department couldn’t allow to forgo such tax revenue and introduced an amended law. (obviously duh…)

Introduction of the new clause under Section 6 IA created a lot of panic among expatriates living abroad. But there isn’t anything to worry about as India has a Double Taxation Avoidance Agreement (DTAA) with most countries.

For Example…

- Fatema is a Resident of the USA and India and has an Economic Interest in the US, but also enjoys Income from shares (LTCG) in India. In that case, She will need to pay tax on LTCG in India. She can get a rebate for the same amount when she files her return in the US. Adding on, any income she earned in the US will not be taxed in India as per the DTAA.

- The second Scenario, If her permanent home is in the US, then Fatema will be only liable to pay taxes there. But in case Fatema is having a permanent home in both the countries, Tax will be deducted in the country where she has Economic Interest.

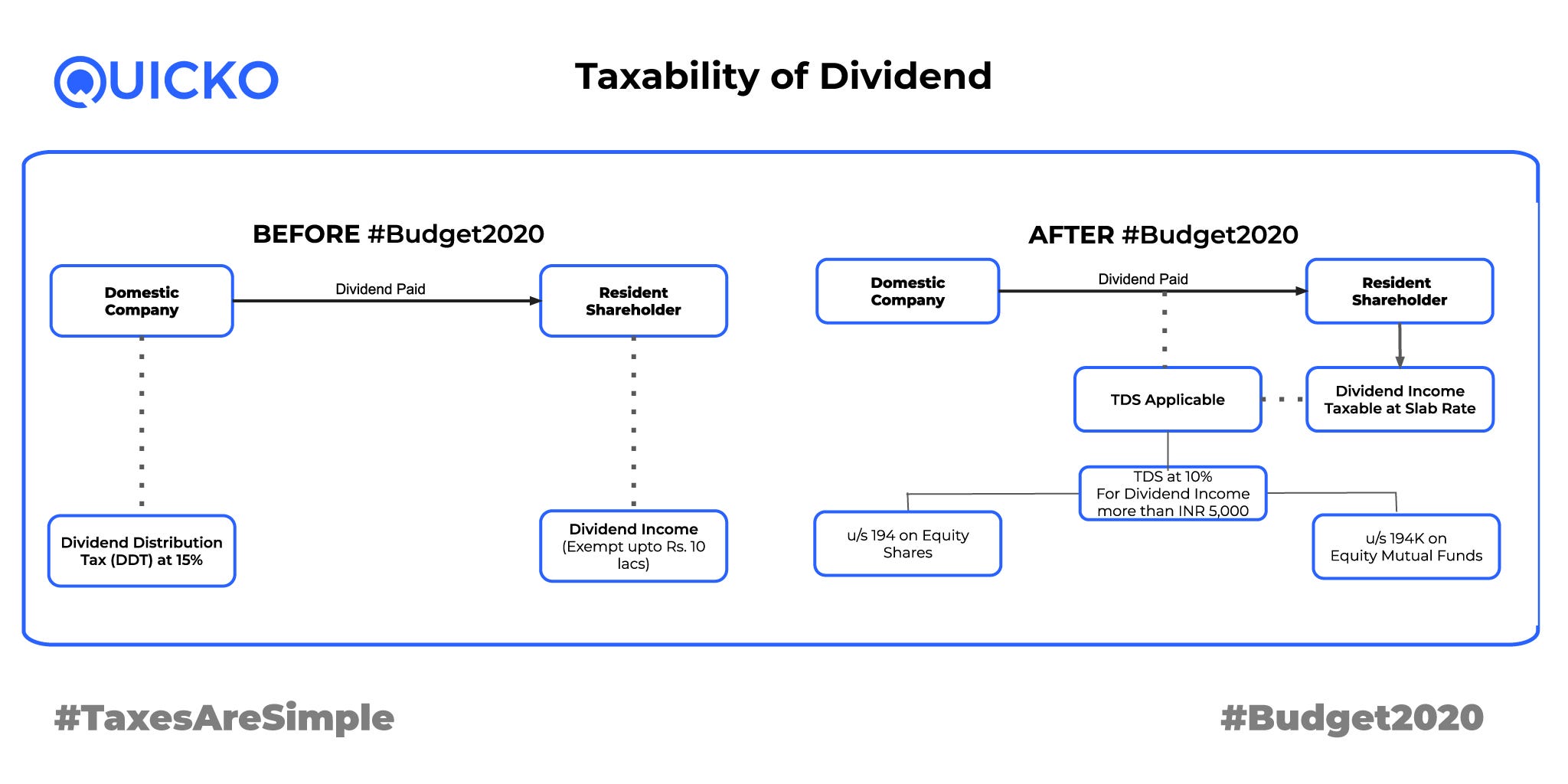

Dividend Distribution Tax (DDT) for NRIs

Up to FY 19–20, DDT was deducted by the companies on dividend paid to its shareholders. In the Finance Bill, FM Nirmala Sitharaman abolished DDT paid by the companies. The Dividend is not taxable in the hands of the shareholders. However, companies will deduct TDS on dividend distributed.

As the old saying goes, “One never forgets one’s roots” many Indians living overseas hold shares of Indian Companies. Since there is no DDT, TDS will be applicable to Investors. TDS will be deducted u/s 195 in the case of NRI shareholders and dividend income will be taxed at slab rates.

NRI’s can claim a refund of deducted TDS by filing ITR. With this change, the Income Tax Department is expecting an increase in the number of foreign investors. Hence, reviving the slow Investment rates in the country.

Refer to the image below for further clarity…

To wrap up, it looks like FinMin has had her patience tested with Individuals who dodged paying taxes. With these changes, she has made it clear that the Indian Government will not allow Residents to run loose. While she tried to make sure that no one is treated unfairly or pays double taxes. We feel that these changes will help to limit the outflow of unregistered Income and help to curate it for the greater good.